UnitedHealth Group (NYSE: UNH) is mounting a decisive recovery, marking a sharp reversal from one of the most significant drawdowns in large-cap healthcare.

In April 2025, the stock collapsed roughly 50% following a surprise earnings miss and weak guidance, triggering widespread concern over margin pressure and the sustainability of growth across managed care.

Almost exactly one year later, that narrative is shifting. UNH shares have climbed roughly 28% over the past 30 days in the stock market, with momentum accelerating into the company’s latest earnings release.

Earnings beat resets the investment narrative

The primary catalyst behind the latest move higher is a material earnings beat that has begun to restore confidence in UnitedHealth’s execution.

The company reported $111.72 billion in revenue, exceeding expectations by more than $2 billion, while earnings per share came in at $7.23 versus $6.57 expected.

More important than the headline beat was what it signaled. After months of concern around cost pressures, particularly in Medicare Advantage, the results pointed to stabilizing margins and improved operational control.

The market response was immediate. UnitedHealth shares surged in extended trading from a $323.48 close to around $353 at press time on April 21, reflecting a rapid repricing of near-term expectations.

Policy tailwinds are reinforcing the recovery

The earnings-driven rally is being amplified by a more favorable regulatory backdrop.

Earlier in April, the Centers for Medicare & Medicaid Services finalized its Medicare Advantage update, outlining a 2.48% increase in payments for 2026, equivalent to roughly $13 billion in additional funding. This marked a sharp upward revision from prior estimates and materially improved earnings visibility for insurers.

The impact was evident even before earnings. UnitedHealth shares rose from $281.63 to $323.48 in the two weeks following the announcement, underscoring how sensitive UNH stock is to reimbursement dynamics.

For a company with significant exposure to Medicare Advantage, this shift is not incremental. It directly supports margins, growth, and forward valuation.

Wall Street turns constructive again

With earnings and policy tailwinds aligning, analyst sentiment has shifted decisively.

UnitedHealth stock now carries a Strong Buy consensus on TipRanks, with an average 12-month price target of approximately $368.70, implying further upside from current levels.

More revealing, however, are the three most recent analyst updates, issued between April 20 and April 21, which highlight how the recovery is being interpreted across the Street.

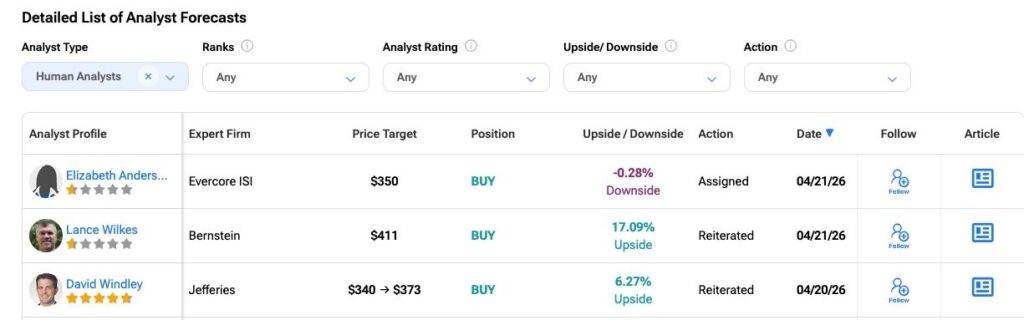

Latest UNH price targets show a market still debating the upside

At Evercore ISI, analyst Elizabeth Anderson assigned a $350 price target on April 21, effectively in line with current trading levels. The call reflects a valuation-aware stance, suggesting that much of the near-term recovery has already been priced in following the sharp post-earnings move.

This is not a bearish view, but it signals caution. Evercore is effectively waiting for continued execution and margin follow-through before turning more aggressive.

That contrasts with Bernstein, where analyst Lance Wilkes reiterated a $411 price target on April 21, implying roughly 17% upside. The firm’s thesis is more forward-looking, centered on margin normalization and improved Medicare Advantage economics extending into 2027.

Bernstein’s view suggests the market is still underestimating the earnings power recovery cycle, particularly as policy support begins to flow through financials.

Between these two sits Jefferies, where analyst David Windley raised his target to $373 from $340 on April 20, implying about 6% upside. Notably, this revision came ahead of the earnings release, indicating that confidence in the recovery was already building before the latest results confirmed it.

UNH stock analyst price targets. Source: TipRanks

Buffett’s positioning reinforces the long-term case

Adding to the narrative is the involvement of Warren Buffett and Berkshire Hathaway. In August 2025, Berkshire disclosed a 5.04 million share stake in UnitedHealth, a move that initially raised eyebrows given Buffett’s long-standing criticism of healthcare costs.

However, the investment aligns with his core strategy of acquiring high-quality businesses during periods of dislocation. With the stock still recovering at the time, the position reflected a classic value entry into a temporarily impaired but structurally strong business.

A convergence of catalysts is driving the rally

What distinguishes UnitedHealth’s current move is that it is not driven by a single factor, but by a convergence of reinforcing catalysts.

Earnings have re-established confidence in execution. Policy changes have improved forward visibility. Analyst sentiment has shifted from defensive to constructive. Meanwhile, institutional positioning has provided an additional layer of support.

This alignment is critical. It transforms the rally from a short-term reaction into a more durable re-rating process.

What comes next for UNH stock

The key question now is whether the recovery can sustain its momentum.

Much will depend on the company’s ability to continue delivering consistent earnings growth while managing medical cost trends. At the same time, the stability of reimbursement policy will remain central to the broader investment case.

For now, however, the trajectory is clear. UnitedHealth is no longer trading as a company under pressure, but as one emerging from it.

And as expectations reset, the recent rally increasingly reflects not just an earnings beat, but a broader shift in how the market is valuing the company’s long-term earnings power.